Foreign company branches are entitled under double taxation avoidance treaties and the Tax Code to deduct head office management and general administrative expenses. These branches are also entitled under treaties to apply a reduced 5% corporate income tax (CIT) rate on net income.

To claim these benefits, taxpayers must provide the tax authority with a document confirming residency. Usually this is a residency certificate apostilled under the 1961 Hague Convention. But between America and Kazakhstan, residency confirmation is done by providing a residency certificate in Form 6166. The mutual agreement between countries specifies that apostilling such certificates is not required.

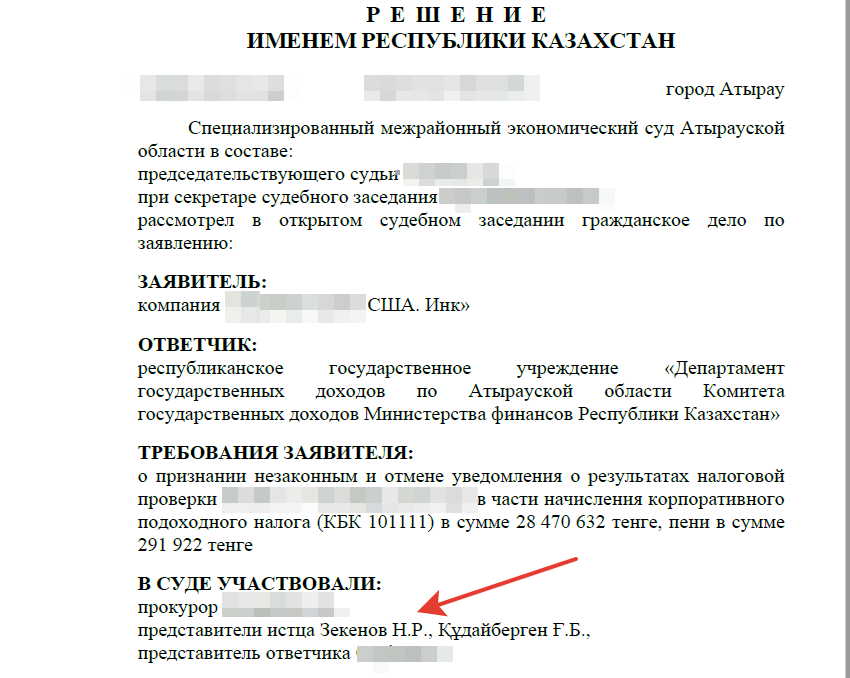

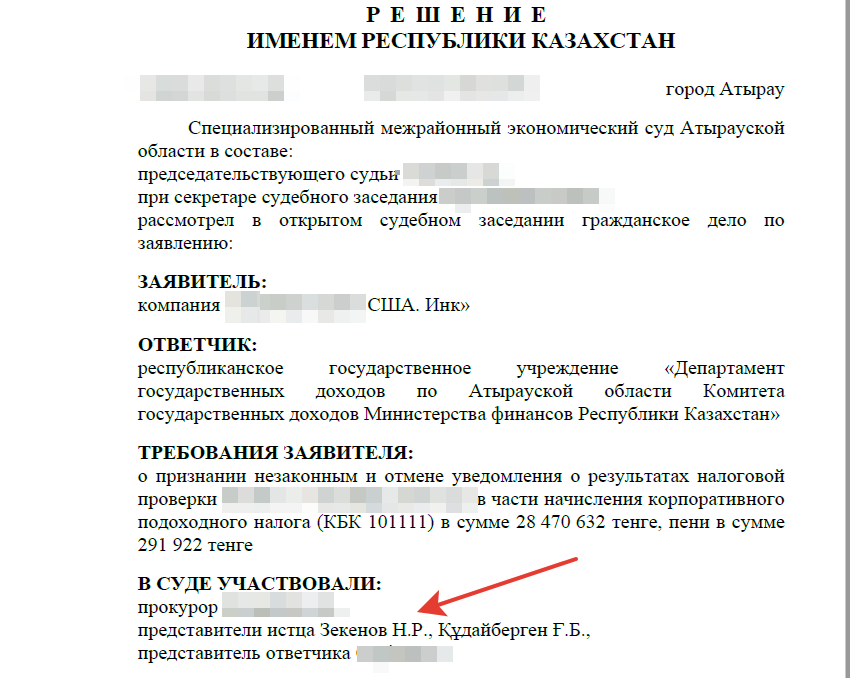

During an audit of the American company's branch, the tax authority expressed dissatisfaction with the certificate formatting. They consequently excluded head office management and administrative expenses from deductions and applied the maximum 15% CIT rate on net income.

There were also assessments on other grounds caused by the taxpayer's own errors. The client approached us to resolve this issue. To avoid additional state duty costs, we suggested the client appeal only the portion we described. The rest was hopeless.

The CIT amount assessed on this basis was 28.4 million tenge, with penalties of 291 thousand tenge. During the court dispute, Nurlan managed to prove to the court that the submitted certificate met legislative requirements. Consequently, the court declared the assessments unlawful. It was then straightforward to overturn the administrative fine arising from the tax audit totaling 8.5 million tenge.

As a result, in this case Nurlan overturned over 37 million tenge in total.